When you’re comparing stable kit financing Australia options for your equestrian center, have you ever asked a lender whether a portable stable counts as a building or as equipment? The answer most financiers give is the latter — and that changes everything about your monthly payment and tax position. Buyers have often assumed they need a standard commercial property loan, only to discover they could have used a chattel mortgage with a three-year term and a Division 40 write-off instead.

The reason most lenders classify portable stables as plant and equipment rather than buildings comes down to one thing: the kit can be relocated. That classification unlocks faster depreciation, lower interest rates, and for the 2026–26 financial year, instant asset write-off eligibility up to $30,000 — enough to cover a single or double stable kit outright. Some financiers will even require the kit to be assembled within 90 days to qualify as an installed asset, which is worth keeping in mind when you plan the install timeline.

So before you sign anything, it pays to understand how portable stable finance lease Australia structures really work, how hire purchase horse stables Australia stacks up against a chattel mortgage, and which option leaves you with the best cash-flow outcome. Let’s walk through the three common structures and what tax depreciation portable stables actually means for your bottom line.

Why Financing a Stable Kit Makes Sense for Cash-Flow Conscious Operators

Portable kit classification unlocks Division 40 depreciation — most single stables fall under the $30k instant write-off.

Running an equestrian center means managing unpredictable cash flow — feed costs, vet bills, seasonal turnover. Dropping $35,000 on a single stable kit in one payment pulls working capital away from operations. Financing spreads that cost across 24 to 60 months, turning a lump-sum capital outlay into a predictable monthly expense.

- Preserve working capital: Keep cash on hand for feed, farrier, and emergency repairs rather than locking it into infrastructure.

- Tax depreciation: Because portable stables are classified as plant and equipment (not buildings), they qualify for Division 40 deductions including the instant asset write-off. For FY2025-26, the threshold is $30,000 — enough to cover most single and double kits.

- Lower effective cost: Financing interest rates for chattel mortgages on portable stable kits often run 6-9%, which can be offset by the immediate tax benefit of the write-off.

One condition lenders and the ATO share: the kit must be assembled within 90 days of delivery to count as an ‘installed asset’. If it sits in a shed unassembled, it may not qualify for the same depreciation treatment. Plan your installation timeline before signing.

3 Common Financing Structures for Portable Stables

Portable stables qualify as plant and equipment, unlocking faster depreciation and lower rates than building loans.

- Chattel mortgage: You take ownership from day one. The lender holds a lien on the stable kit until the loan is repaid. Monthly payments are higher than a lease, but you claim GST upfront and depreciate the asset under Division 40. Interest rates range from 6–9% depending on your credit profile and the kit’s residual value. Best for operations that want full equity control and plan to keep the stables beyond the loan term.

- Finance lease: The lender buys the stable kit, you lease it back. Lower monthly payments because you only cover depreciation plus interest, not the full purchase price. GST is paid on each lease payment rather than upfront, which helps cash flow. At the end of the term, you can purchase the kit for a residual (usually 20–40%) or return it. Suited for centers that upgrade equipment every 5–7 years and want predictable monthly outgoings.

- Hire purchase: Simplest approval process. You pay a deposit, then fixed monthly instalments over an agreed term. Ownership transfers automatically after the final payment. No residual balloon to manage. Lenders often require the kit to be assembled within 90 days to classify it as an ‘installed asset’ — missing that deadline can reclassify the loan as a building loan with higher rates. Ideal for first-time stable buyers or those with less-established credit history.

Each option affects your tax position differently. A chattel mortgage lets you claim the entire GST credit immediately and depreciate the hot-dip galvanised steel frame (42 microns) and 10mm HDPE panels over their effective life — typically 10–15 years. A finance lease spreads the GST across payment periods but allows you to claim the lease payments as an operating expense. Hire purchase treats the asset like a purchase, so depreciation rules apply after the contract ends. Run the numbers with your accountant against the $30,000 instant asset write-off threshold for FY2026 before deciding.

How Portable Classification Unlocks Tax Depreciation

Portable stables classified as plant & equipment unlock faster depreciation than buildings.

Division 40 of the Australian tax code lets you claim an instant asset write-off for portable stable kits costing under $30,000 in the 2026–26 year. That threshold covers most single and double DIY stable kits. For larger configurations like a back-to-back quadruple, anything above $30,000 goes into a small business pool and depreciates at 15% in the first year, then 30% each year after. The trick? The kit must be installed and ready for use within 90 days of purchase to qualify as an ‘installed asset’ — Lenders and the ATO treat unassembled flat packs sitting in a shed as inventory, not depreciable plant.

- 10mm HDPE panels: Depreciated over an effective life of 10–15 years using the diminishing value method. Because HDPE is UV-resistant and doesn’t suffer thermal expansion, it holds structural value longer—meaning you claim a smaller percentage each year relative to faster-wearing materials. Most accountants apply a 13.33% diminishing rate.

- Hot-dip galvanized steel frames: ATO benchmark effective life for galvanised steel structures is 20 years. With a 42-micron coating and 10-year warranty, these frames typically depreciate at 7.5% diminishing value. The key: you cannot claim the full $30,000 write-off on the frame alone if it’s bundled into a kit over the threshold—allocate cost between steel and HDPE when lodging.

What Lenders Look For in a Stable Kit Purchase

A stable on a concrete slab is a building.

The single most critical distinction in stable kit financing is whether your lender classifies the purchase as a ‘portable asset’ or a permanent building. That classification determines your interest rate, depreciation schedule, and eligibility for the instant asset write-off. In Australia, portable stables are typically treated as plant and equipment under Division 40 of the tax act, not as capital works under Division 43. The difference in depreciation speed is dramatic: 20% to 30% declining value versus 2.5% straight-line.

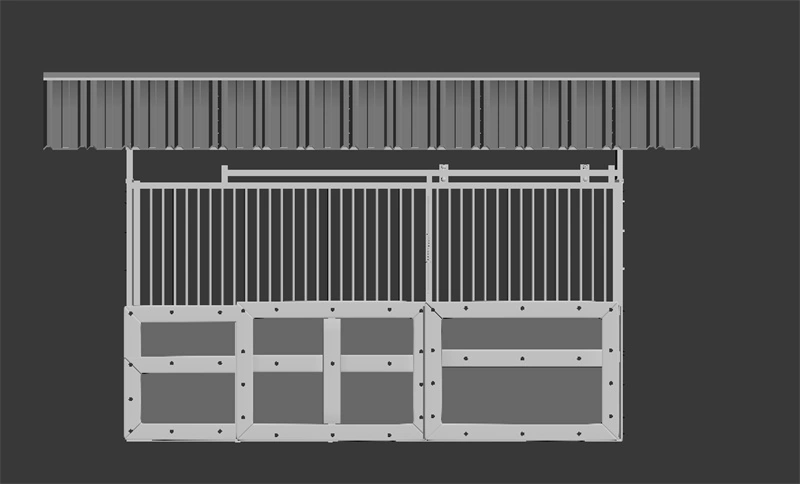

To satisfy a lender that your kit is portable, you need to demonstrate three things: the structure is not fixed to a permanent foundation, it can be disassembled and relocated without destroying its integrity, and it was manufactured as a prefabricated system — not a custom build. DB Stable’s flat-pack design with bolted hot-dip galvanized steel frames and HDPE panels meets all three criteria. The same kit that qualifies for a chattel mortgage or finance lease would fail lender criteria if it were bolted into concrete footings.

- No permanent foundation: Lenders will inspect for concrete footings, slab attachments, or in-ground posts. A portable stable sits on compacted gravel or timber sleepers — removable in hours.

- Assembly timeline: Some financiers require the kit to be assembled within 90 days of delivery to qualify as an ‘installed asset’. If you plan to delay installation, disclose this upfront or risk the loan being reclassified.

- Manufacturer documentation: A stamped compliance certificate from the supplier (DB Stable provides these on request) proving the kit is a standard manufacturer model, not a permanent fixture, is often enough to secure the lower equipment rate.

- Resale and relocation ability: Lenders may ask for a valuation that confirms the stable can be sold separately from the land. A modular kit that can be unbolted, flat-packed, and moved retains asset value much better than a built-in structure.

The $30,000 instant asset write-off threshold for the 2026-26 financial year covers most single and double stable kits outright. But that benefit only applies if the asset is classified as portable plant and equipment. If your lender slaps a ‘building’ label on it, you lose the write-off and the depreciation drops to a crawl. Always ask your finance provider to confirm their classification in writing before you sign.

Real Example: Financing a 6-Stall Back-to-Back Kit

A $45,000 kit: lease payments $890/month vs mortgage $1,150/month.

Let’s run numbers on a 6-stall back-to-back kit from DB Stable. At FOB pricing of roughly $45,000 delivered to an Australian port (excluding GST), your financier will classify the kit as plant and equipment, not a building. That classification directly affects your monthly outlay and your tax position.

- Chattel mortgage (5-year term, 7.5% rate): Monthly payments approximate $1,150. You own the asset from day one, claim depreciation under Division 40, and can sell or relocate the stables without refinancing.

- Finance lease (5-year term, 8% rate, 25% residual): Monthly payments around $890. You never take legal ownership, but the lower payment preserves cash for other capital. Plus, the GST is spread across the lease term instead of being claimed upfront.

- Key catch: 90‑day assembly rule: Some lenders require the kit to be fully assembled within 90 days of delivery to qualify as an ‘installed asset’. If your crew takes longer, the financier may reclassify the kit as uninstalled goods, bumping the rate by 1–2 points.

Steps to Get Pre-Approved Before You Order

Pre-approval hinges on proving the stable is portable equipment, not a building.

To get pre-approved for stable kit financing, you’ll typically need three documents: a formal quote from the supplier, your ABN or business registration, and two years of financial statements. The formal quote must explicitly list the kit as ‘portable’ or ‘flat pack’ — if it reads like a building contract, lenders may classify it as real property and bump up the interest rate. Your ABN confirms you operate a business (essential for the instant asset write-off), and your financials show the lender you can service the repayments. For 2026-26, the instant asset write-off threshold sits at $30,000 for small businesses (turnover under $10 million), covering most single and double stable kits.

- Formal Quote: Must break down the kit into components (frames, panels, roof) and clearly state the kit is ‘portable’ or ‘flat pack’. Lenders use this to classify the asset as plant and equipment under Division 40, unlocking faster depreciation and lower rates. Avoid quotes that lump everything as ‘building materials’.

- ABN / Business Registration: Required for any commercial financing. Lenders want to see the business entity (sole trader, partnership, company) that will own the stable. If you’re a farm owner running an equestrian centre, your ABN-linked business name should match the quote and the land title if the stable will be used for income-producing activities.

- Financial Statements / Tax Returns: Last two years of profit & loss and balance sheet, or tax returns if self-employed. Lenders look for consistent cash flow and a clear business purpose for the stable. If your annual turnover is under $10 million, you’re eligible for the instant asset write-off — but only if the asset is installed and ready for use by 30 June 2026.

One detail most buyers miss: some financiers require the stable kit to be assembled within 90 days of delivery to qualify as an ‘installed asset’. If your installation drags beyond that window, the lender may reclassify the finance as a standard loan with a higher rate. A few lenders also request a supplier declaration confirming the kit’s FOB value and origin — especially if you’re importing DIY flat packs from a manufacturer like DB Stable. Missing that document can delay draw-down by weeks.

Insider warning: if you’re planning to self-fund and claim depreciation later, you still need a formal depreciation schedule from a qualified quantity surveyor. Many centre owners pay cash for a $40,000 stable kit, then forget to depreciate the HDPE panels and galvanized steel separately under Division 40. That’s thousands in missed deductions. Get the schedule prepared at the time of purchase, not at tax time.

Conclusion

Financing a stable kit through chattel mortgage, lease, or hire purchase only works if the asset qualifies as portable plant and equipment — not a building. That classification unlocks Division 40 depreciation and keeps the lender comfortable. Before you sign anything, run these three checks against your supplier and your own setup.

Decision Checklist 1. Does the supplier provide a clear depreciation schedule showing the 10mm HDPE panels and galvanized steel frame as separate depreciable components? 2. Can the supplier confirm in writing that the kit is designed as a non-permanent structure, with no concrete foundations required, making it eligible for ATO portable asset classification? 3. Does your timeline allow for site preparation and assembly within 90 days of delivery — the window most financiers require to treat it as an installed asset? If you answer yes to all three, you’re in a strong position. Review your stable kit quote with these checks in hand. If the answers are clear, you’re ready to proceed.

Frequently Asked Questions

Does a portable stable count as equipment for financing?

Yes, portable stables qualify as plant and equipment rather than a building, which unlocks faster depreciation and lower interest rates. Lenders look for proof that the kit is truly portable—not permanently fixed to foundations. Get a quote that specifies portability before applying.

What financing structures are available for stable kits?

The three common structures are chattel mortgage, finance lease, and hire purchase, each with different ownership and GST benefits. Chattel mortgage gives ownership from day one, while finance lease offers lower monthly payments. Compare monthly payments for your kit size before choosing.

How does portable classification unlock tax depreciation?

Portable stables fall under Division 40, allowing instant asset write-off if the cost is under the 2026 threshold. The 10mm HDPE panels and hot-dip galvanized steel can be depreciated on a schedule. Check current ATO instant asset write-off limits with your accountant.

What documents do lenders need for stable kit financing?

Lenders typically require a formal quote, your ABN, and recent business financials to assess cash flow. Proving the kit is a portable asset rather than a permanent structure is also critical for approval. Prepare these three documents before you apply.

Can I get pre-approval before ordering a stable kit?

Yes, most lenders offer pre-approval based on your financials and the kit quote, helping you lock in terms before placing the order. Pre-approval typically requires the same documents—quote, ABN, and financials—and is. Submit your quote and ABN to start the pre-approval process.